Introduction to the Bank of England Base Rate

The Bank of England Base Rate is a critical economic indicator that influences borrowing and saving across the United Kingdom. Its movements affect inflation, consumer spending, and the overall economic stability of the country. As of 2023, many are closely monitoring these changes given the ongoing economic challenges and recovery from the pandemic.

Recent Developments

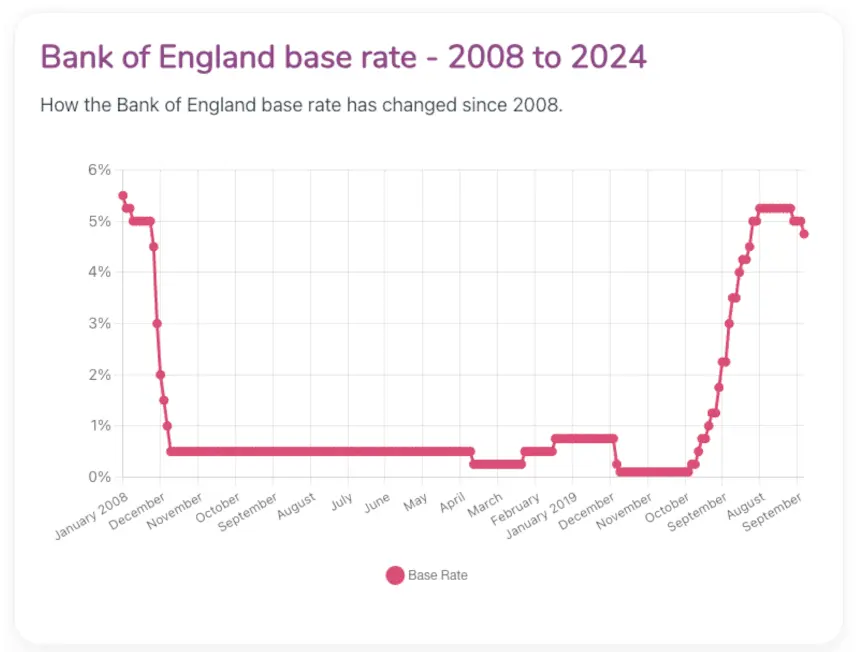

As of September 2023, the Bank of England’s Monetary Policy Committee (MPC) announced a maintained base rate of 5.25%, marking a period of stability after a series of increases aimed at curbing inflation. In recent months, the MPC has had to balance the need to combat rising prices with the risk of slowing down economic growth. In August, the consumer price index showed a slight decrease in inflation, coming in at 5.2%, a positive sign yet still above the Bank’s target of 2%.

The Bank has indicated that while inflation pressures remain, the rate of increase appears to be stabilising. A primary concern identified is the potential impact of higher borrowing costs on consumer spending, a significant driver of the UK economy. Recent surveys suggest that households are tightening their budgets in response to increased mortgage and loan repayments.

Impact on Borrowers and Savers

The base rate affects a plethora of financial products, including mortgages, savings accounts, and loans. Higher rates typically lead to increased borrowing costs, which can particularly impact those with variable-rate mortgages. Homeowners may find themselves facing increased monthly payments, leading some experts to warn of a potential rise in defaults if the economic situation does not improve. Conversely, for savers, the increased base rate usually heralds higher interest on savings accounts, which has been a long-awaited reprieve after years of low returns.

Conclusion and Future Projections

Looking ahead, the Bank of England has signalled that it remains cautious about making further increases in the base rate. Economists speculate that any future adjustments will depend heavily on inflation trends. If inflation continues on a downward trajectory, the Bank may consider lowering the base rate again by mid-2024 to support economic growth. However, should inflation remain stubbornly high, further increases may be necessary.

The outcome of these decisions will be pivotal for the UK economy, affecting everything from mortgage payments to borrowings for businesses. It is essential for consumers and investors to stay informed as the Bank of England continues to navigate these challenging economic waters.