Introduction

The Bank of England base rate is a key instrument of monetary policy, influencing borrowing and saving costs across the UK. Recently, the rate has been in the spotlight as inflationary pressures continue to challenge the economy. Understanding the developments surrounding the base rate is essential for consumers, businesses, and investors alike.

Recent Developments

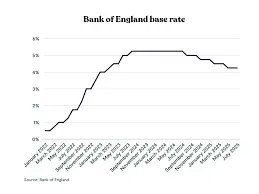

As of October 2023, the Bank of England’s Monetary Policy Committee (MPC) has maintained the base rate at 5.25%, a decision made during its latest meeting on October 5. This rate has raised eyebrows given the ongoing fears of inflation, which remains stubbornly high at around 6.7% despite indications of a moderate slowdown in economic growth.

The base rate, which was significantly increased in 2022 to combat rising inflation, is closely monitored for its ripple effects throughout the economy. The Bank aims to balance the need for consumer spending and growth against the necessity of controlling inflation. Thus, the current base rate is a signal of the institution’s commitment to achieving its target inflation rate of 2%.

Impact on the Economy

The ramifications of the base rate on the economy are profound. A higher base rate typically means increased borrowing costs for mortgages, loans, and credit cards, which can dampen consumer spending and investment. Furthermore, businesses may face higher funding costs that can lead to reduced hiring or even layoffs as they reassess financial strategies.

Conversely, for savers, a higher base rate offers the potential for improved returns on savings accounts and fixed-income investments. However, the overall economic climate, including wage growth, tax policies, and global economic conditions, plays a significant role in determining the effect of the base rate on individuals and businesses.

Future Outlook

Looking forward, analysts and economists are divided on the future movements of the base rate. Some predict that if inflation continues to show stubbornness, the Bank may need to raise the base rate further to curb excessive price rises. Others suggest that a downturn in economic growth could lead to a pause or even cuts in rates if inflation shows consistent signs of easing.

Ultimately, the decisions made by the Bank of England in the coming months will be closely watched as they will not only impact the domestic economy but also influence market confidence and the broader financial landscape.

Conclusion

The Bank of England base rate remains a critical element of the UK’s economic strategy. As consumers and businesses adapt to the current economic climate, understanding how the base rate affects different aspects of financial life is ever more important. Staying informed about these developments can empower individuals and enterprises to make better financial decisions in the months ahead.