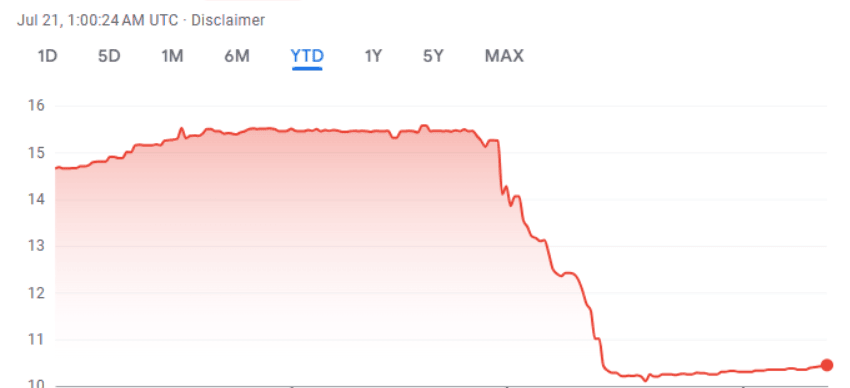

A person searching this question usually wants a quick idea of the current local value of 1 USD, but the answer is not always one fixed number. The Ghanaian cedi value can change during the day, and different providers may show different figures at the same moment. A central bank quote, a commercial bank card rate, a forex bureau board and a mobile money or payment app screen can all point to slightly different outcomes. The useful answer is therefore not only “what is the rate today,” but also “which rate applies to my situation.” This guide explains how to read the value, why it changes, and how to compare sources before travel, remittances, online payments or business planning.

Why the rate changes before you convert money

Currency value moves because buyers and sellers constantly react to supply, demand, inflation expectations, import needs, interest rates, foreign reserves and wider market sentiment. When demand for dollars is high, the local cost of buying dollars can rise. When more foreign currency enters the market, pressure may ease and the displayed amount can move in the other direction. Public converters often track broad market data, while real transaction channels add their own costs. That is why the rate shown in a news article or converter may not match the amount a person receives from a bank, bureau, card issuer or transfer provider.

Why timing can change the final cedi amount

Timing also matters. A quote checked in the morning may not be the same as a quote used when a payment settles later. For large transfers, even a small movement can change the final Ghanaian cedi amount. For everyday users, the safer habit is to compare the displayed rate, the fee and the final receivable value together. Looking only at the headline number can make one provider look better than it really is.

Where 1 dollar to Ghana cedis values come from

A basic converter can help the user understand direction, but it should not be treated as the final transaction amount. The conversion figure on a converter is usually a reference point, not a promise from a bank or money transfer service. A commercial bank may apply its own spread when a card payment is processed. A forex bureau may publish a cash buying and selling quote that reflects local supply and demand. A mobile money or payment app may include provider margin, transfer fees or rounding. The same comparison can therefore produce several practical answers depending on where the conversion happens.

| Source type | What it usually shows | Why it may differ | Best practical use |

| Central bank or official quote | A formal reference rate | It may not include retail spreads or transaction fees. | Useful for context, reporting and macro comparison. |

| Commercial bank | Card, transfer or account conversion value | Bank margin, service fee or settlement timing may apply. | Useful before card payments, invoices and account transfers. |

| Forex bureau | Cash buy and sell values | Local cash demand, supply and bureau spread affect the quote. | Useful for travel cash and walk-in currency exchange. |

| Mobile money or payment app | Displayed transfer or payment value | Provider fee, wallet rules or rounding may change the final amount. | Useful for remittances, small payments and quick transfers. |

Official rate, bank rate, bureau rate and market rate explained

The official rate is usually a reference figure used for reporting, policy context and market direction. It helps users see the general value of the currency pair, but it may not be the rate available at a counter or inside a banking app. A bank rate is more practical for card users and account holders because it reflects how a commercial bank prices the transaction. It can include a spread, a service charge or a card-network conversion step. A forex bureau rate is often more relevant for cash because the bureau needs to manage physical currency supply, demand and operating margin.

What market rate really means in practice

The market rate is a broader phrase and can mean different things depending on context. Sometimes it refers to interbank or wholesale pricing, and sometimes people use it informally to describe the going retail value outside official channels.

- Interbank rate: The value used between banks or large financial institutions, usually not available to ordinary retail users.

- Wholesale rate: A broader reference level used for larger currency transactions, often before retail margins are added.

- Retail market rate: The practical value a customer may see at banks, forex bureaus or payment providers.

- Informal market quote: A local estimate people may use in conversation, but it should be checked against a reliable provider.

This is why US dollar to cedis comparisons should always name the source. Without that source, the figure can be technically true but practically incomplete.

Official quote as a reference point

An official quote is useful when the user wants a formal benchmark. It can help with accounting assumptions, economic reading and general direction. However, it normally does not show every charge a retail user may face. The official number should be read as a starting point rather than the final amount in hand. For a real payment, the user still needs to check the provider that will process the transaction.

Bank and card rates for real transactions

A bank rate matters when the user pays online, receives funds into an account or uses a card abroad. The bank may convert at the moment of authorization, settlement or posting, depending on the transaction type. That timing can create a small difference between the expected amount and the statement value. Some banks also add foreign transaction fees or service charges. The final cost is therefore a combination of rate, fee and processing rule.

Forex bureau and cash-market context

A bureau may show two figures: one for buying foreign currency and one for selling it. The selling price is usually what a customer pays to buy dollars, while the buying price is what the bureau pays when receiving dollars from the customer. The gap between the two is the spread, and it helps the bureau cover risk and operating costs. Cash availability can also affect the quote, especially when demand changes quickly. Users comparing cash options should ask for the final amount before handing over money.

How to compare USD to GHS values in everyday situations

The most practical comparison is not always the provider with the highest headline number. The better choice is the provider that gives the best final value after fees, spread, timing and reliability are considered. For small payments, convenience may matter more than a tiny rate difference. For business invoices, remittances or travel budgets, the final receivable amount can be more important.

- Source: Check whether the quote comes from an official reference, bank, bureau, payment app or converter.

- Direction: Confirm whether the provider is buying dollars, selling dollars or converting a payment.

- Spread: Compare the gap between buy and sell values where both are shown.

- Fee: Add transfer charges, card fees, service costs or cash-handling costs to the calculation.

- Timing: Check whether the rate is locked immediately or can change before settlement.

- Final amount: Focus on what the receiver gets or what the payer is actually charged.

- Record: Keep the receipt, transfer screen or statement when the transaction value matters.

This order helps the user avoid comparing a clean reference quote with a real transaction quote that includes added costs.

Practical examples for travel, remittances and online payments

For travel, a visitor may compare a bureau quote with a bank card quote. The bureau may be useful for cash needs, while the card may be easier for hotels, online bookings or larger purchases. The right choice depends on fees, acceptance and the amount of cash required. A traveler should avoid judging value from a single public converter. The local value becomes clearer only after the provider shows the final amount.

Remittance costs and final received value

For remittances, the sender should check both the exchange rate and the transfer fee. A service may advertise a strong 1 USD to GHS value but charge more for delivery. Another provider may show a slightly lower rate but deliver more after fees. This is where USD to cedi comparison becomes practical: the best result is the amount received, not only the rate displayed. Delivery speed and payout method can also matter if the receiver needs funds quickly.

Online payments, card issuers and billing currency

For online payments, card networks and payment apps may use their own pricing. The card issuer may convert later than the moment the user checks a converter. The statement may also include a separate international fee. A business paying suppliers should confirm whether the invoice is billed in dollars or settled in Ghanaian cedis. Clear billing currency reduces confusion when the posted amount appears.

Why the displayed amount can differ from the final received value

A displayed amount can differ from the final value because each provider manages risk and cost differently. Spreads protect providers against market movement. Fees cover processing, transfer networks, cash handling or card services. Timing matters because a rate may be estimated before the transaction is fully settled. Rounding can also affect small payments, especially in apps or wallets. The exchange rate dollar to cedi should therefore be read together with the provider’s full price, not as an isolated number.

Indicative and guaranteed rates before confirmation

Users can reduce surprises by checking whether the rate is indicative or guaranteed. An indicative rate is an estimate and may change before completion. A guaranteed rate is usually locked for a short period, but it may come with conditions. The receipt or confirmation screen should show whether charges are included. When the amount is important, the user should compare at least two practical channels instead of relying on only one converter.

| Pros | Cons |

| Indicative rates help users estimate the possible cost before starting a payment, transfer or currency exchange. | The displayed figure can change before completion, so the final amount may be different from the early estimate. |

| Guaranteed rates give clearer short-term certainty when the user needs to know the exact payable or receivable value. | A locked rate for one dollar in Ghana cedis may be available only for a limited time and can expire before the transaction is completed. |

| Checking the confirmation screen helps users see whether fees, spreads or service charges are included in the final value. | Some providers show attractive headline rates but add separate charges later in the payment flow. |

| Comparing at least two channels makes it easier to identify whether one provider’s quote is unusually weak or expensive. | Comparing rates can take more time, especially when banks, bureaus and apps update their figures at different moments. |

Common mistakes when reading dollar to cedi values

One common mistake is comparing an official quote with a retail cash quote and assuming one of them is wrong. They may simply serve different purposes. Another mistake is ignoring whether the provider is buying or selling dollars. A third mistake is looking at the rate but not adding the fee. Users can also misread card transactions because authorization and settlement may happen at different times. The safest approach is to compare total payable and total receivable values in the same direction.

FAQ about exchange rates between the dollar and Ghana cedis

Is how much is one dollar in Ghana cedis the same at every provider?

No, it is not the same at every provider. An official reference, a bank app, a bureau counter and a payment service may all use different pricing rules. The best comparison is the final amount after spread, fee and timing are included.

How often should I check the rate?

A user should check the rate close to the time of the transaction. Currency values can move during the day, and providers may update their screens at different moments. For larger transfers or business payments, checking more than one source is a practical habit.

What is the difference between official and market rates?

The official rate is a formal reference, while market pricing can reflect real buying and selling conditions across banks, bureaus or broader trading. Retail users usually cannot assume that a formal benchmark is the exact value available for cash or payments. The practical figure depends on the provider used for the transaction.

Why does my card statement show a different amount?

A card statement can differ because the issuer may use a later settlement rate, add a foreign transaction fee or process through a card network. The USD to GHS value seen before payment can therefore be only an estimate. The statement value is the confirmed amount after the card issuer applies its rules.