Introduction

The UK state pension age is a crucial topic for millions of citizens approaching retirement. It determines when individuals can begin receiving their pension benefits, directly impacting their financial planning and quality of life. As life expectancy rises and the economic landscape changes, adjustments to the state pension age have become increasingly significant, making it essential for individuals to stay informed about any updates.

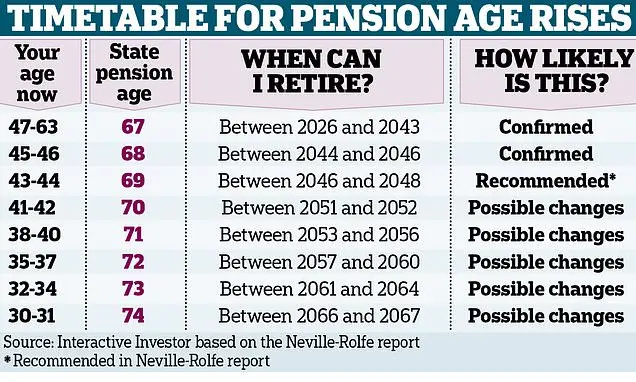

Recent Changes to the State Pension Age

According to the latest government announcements, the state pension age for both men and women is set to increase to 67 years by 2028. Previously, the age was gradually increasing from 65 years, reflecting a broader trend across many developed nations that seek to maintain pension sustainability in the face of an ageing population. The decision aligns with the government’s commitment to ensuring the longevity of the pension system while also addressing concerns about the economic implications of an ageing workforce.

Impacts on Retirement Planning

The changes to the pension age not only affect when individuals can retire but also influence how they plan for their retirement. Citizens need to reassess their financial strategies, taking into account the new eligibility dates. Moreover, early retirement plans or schemes may require adjustments, and individuals should consider consulting financial advisors. The timing of contributions to pension plans and savings is now more critical than ever, as individuals may need to work longer to secure a comfortable retirement.

Public Reactions and Concerns

The announcement has elicited mixed responses from the public. While some understand the necessity of increasing the pension age given longer life expectancies, others voice concerns over the implications for those in physically demanding jobs, who may find it challenging to work until the new age limits. There have been calls for more tailored support for workers in strenuous professions.

Looking Ahead: Future Implications

The potential plans to further increase the pension age beyond 67 in the 2030s are already generating discussions among policymakers and economists. Although these measures aim to sustain the pension scheme, they also reflect the ongoing debate over retirement security and workplace resilience. Citizens are advised to stay informed about policy developments and adjust their preparedness accordingly.

Conclusion

The changes to the UK state pension age represent a significant shift in how the government is addressing demographic changes. As the landscape continues to evolve, citizens must remain proactive in managing their retirement planning. Understanding these shifts is vital for ensuring financial stability and security in retirement.